A $40 billion market glitters on the horizon, operators and investors are dazzled, but two new reports argue that a reality

Abody of persuasive financial opinion has emerged in recent weeks to suggest the industry should take the opportunity of a reported delay in passage of Japan’s casino legalization to take a breather and rethink some of the more outsized forecasts in terms of gaming revenue and return on investment.

Morgan Stanley analysts Praveen Choudhary and Alex Poon returned from a recent trip to the country to add a new report to the bank’s “Asia Insights” series soberly titled “Japan — Tempered Enthusiasm” in which they advance a decidedly less optimistic view of the timing of the market’s debut and its ability to draw enough foreign tourists—Chinese high rollers, in particular—to justify the top-line projections that have excited so much interest worldwide among operators, shareholders and the media.

They begin by stating, “We believe that consensus may be too bullish on the size of the market, the return profile for global gaming operators, and the speed of execution.”

They follow with 23 pages of detailed analysis, co-written with the bank’s Thomas Allen in New York, culled in part from meetings with policymakers, consultants and various stakeholders which they say have left them “incrementally negative on the prospects for the passing of an introduction bill this summer and an implementation bill over the next two years, to get casinos ready by 2020”.

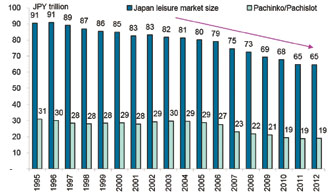

Leisure and Pachinko/Pachislot Markets Are Declining in Size

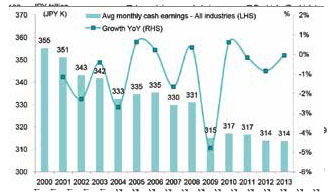

Spending Power of Japanese Citizens Has Been Falling

Spending Power of Japanese Citizens Has Been Falling

The prevailing view is that a bill introduced in the Diet in December to decriminalize the industry will be debated this month and passed before the chamber adjourns on 22nd June, setting the stage for a follow-up bill addressing the thornier issues of regulation, taxation and licensing which will be finalized and passed over the next year or so. It’s a view that stems from Prime Minister Shinzo Abe’s reputed support for legalization as a tool for raising Japan’s profile as a tourist destination in aid of the larger economy, which has been stagnant for decades. Bolstering this is the view that the bill enjoys broad support in the Diet based on its origins as a coalition effort led by top lawmakers within Mr Abe’s Liberal Democratic Party backed by the LDP’s allies among some influential smaller parties, a combination that holds decisive majorities in the Diet and the upper House of Councillors. Then there is Tokyo’s selection to host the 2020 Summer Olympics, which has stoked the political momentum, or so advocates claim, and has supplied a ready-made calendar for dating the first openings.

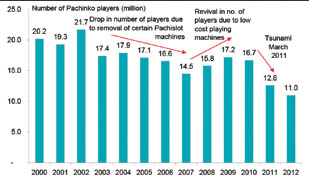

Number of Players Drooped by 50% Between 2002 and 2012

Messrs Choudhary, Poon and Allen rate the authorization bill’s chances at better than 50%. But underscoring recent news reports of a possible delay in scheduling the debate they caution that the backroom wrangling that naturally accompanies legislation this significant (consensus-building, as it’s politely known in Japan) could take longer to resolve than the above timetable suggests, especially given a long history in Japanese society of ambivalence toward casinos.

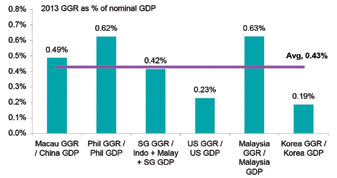

Casino Gross Gaming Revenue as Percent of Nominal GDP

“If there is not enough time to debate, then the vote could be postponed to the fall or next year—and by then, the momentum could be lost,” they write.

The ensuing process of structuring the market will be even more complicated, with many moving parts to be aligned that must take into consideration the primacy of the prefecture system in Japan’s highly federalized political system and the need to satisfy a plethora of special interests, national and local.

The Highest Casino GGR to Lottery GGR Ratio is 3.0x

In all, they say, the consensus belief in a 12-month window for implementation “may be too optimistic”.

“We see several steps to be taken, many new agencies to be created, and consensus to be built on the size of the tax, use of junkets, tax deductibility of incentives, number of casinos, locations, participation by local companies, and safeguards for the local people. We see no real pressure for casinos to be ready before the 2020 Olympics, as consensus has highlighted.”

RelatedPosts

What’s riveted the industry’s attention, though, is the US$40 billion in projected gross gaming revenue, which if it pans out will see Japan grow over the next decade into the second-largest casino market in the world. It’s based on a forecast of $8 billion each for two megaresorts in Tokyo and Osaka and another $2.4 billion each from 10 smaller regional casinos. The Morgan Stanley analysts have their doubts. They point to weaknesses in Japan’s overall appeal as a destination, particularly with regard to visitation from China. The ability to attract Chinese high rollers is essential to fostering a Macau-like VIP market, in their view, and it’s a prospect they rate as questionable, especially if the regulatory line on junkets is drawn closer to Singapore’s than to Macau’s, which is likely.

The Locals: a Closer Look

It’s an argument seconded in its essentials by Chris Jones, senior Gaming & Lodging analyst for Telsey Advisory Group, a consumerfocused brokerage based in New York. He’s written an even longer report that also zeroes in on the slow progress the country has made in meeting the government’s tourism goals. Japan has set a target of 18 million visitors in 2016 and 25 million in 2020, but it has yet to attract even 10 million, in light of which, comparisons with Singapore largely fall away, in his view, considering that the tiny city-state draws 15 million visitors annually. Nor does he believe the allure of the 2020 Olympics will be enough to redress the shortfall. Nearby competition could also arise to dent the potential, he says, especially if Korea responds by opening its casinos to domestic play.

He also questions the prospects for significant growth from an underserved domestic market, an assessment that figures prominently in Morgan Stanley’s research as well. Mr Jones notes that Japan’s population is expected to shrink from 128 million today to 97 million by 2020. Messrs Choudhary, Poon and Allen, for their part, point to the limited impact of Japanese gamblers worldwide, to declining trends in pachinko revenue and to challenges the industry is likely to encounter in converting the country’s massive market of pachinko players into slot machine players.

Both firms take a top-down approach that looks at GGR in relation to nominal GDP to arrive at estimates of annual revenue in the realm of $16.5 billion to $23.8 billion (Jones) and $21 billion-$22 billion (Choudhary, Poon, Allen). The former’s low-end estimate comes in well below consensus in projecting a combined $10 billion from two casinos in Tokyo, $3.8 billion from a casino in Osaka and as much as $1.8 billion each from casinos in Hokkaido and Kyushu.

The Morgan Stanley team qualify their estimate as a best-case scenario, implying they might not disagree with Mr Jones at his most conservative.

To quote the basics of their argument for using GDP as an indicator: “The average is about 0.43% in Asia and US gaming markets,” they write. “If we apply this percentage to Japan’s 2013 nominal GDP of US$4.9 trillion, Japan’s GGR would be roughly US$21 billion, only half of the market consensus of US$40 billion. Even more importantly, this could be divided among 10-12 casinos across Japan and thus the Tokyo market’s GGR could be as low as US$5-6 billion (though impressive in the context of Las Vegas/ Singapore, which are US$6-7 billon markets).”

They also offer a bottom-up analysis, looking at GGR as a ratio of lottery turnover—a “good indicator of how big the gambling business could be,” they say.

“Singapore has the highest GGR to lottery turnover ratio among Asian gaming markets at 3.0. If we apply Singapore’s payout ratio to Japan’s drop of US$11 billion, we come to Japan lottery revenue of US$7.26 billion, implying casino GGR of US$21.8 billion. Considering the lottery business is much closer to mass (but not VIP), a ratio of 1.6x would imply mass revenue of US$12 billion. With a lower VIP revenue mix in Japan due to fewer Chinese players and potentially no junkets, overall GGR could be even lower than US$21.8 billion.”

They note that bulls frequently point to the enormity of Japan’s pachinko market (US$36 billion in 2012) as an indicator of revenue potential, but here, too, they take a contrarian view. “[The market] has been declining for the last several years,” they note, citing steadily falling handle dating back to 1996 and, since 2009, a decline in the average number of players per machine. As they see it, both are reflective of declines which they’ve observed in the earnings of Japan’s leisure sector overall over the last several years and the spending power of Japanese consumers.

“Secondly, not all pachinko players will transplant to casinos when they open,” they contend. But assuming 20% do, they arrive at a Tokyo slot market worth $1.2 billion based on $5 billion in current pachinko revenue—a market, interestingly enough, that would be smaller than Macau’s ($1.78 billion in 2013).

Their conclusion is that companies banking on 20% ROIC in Japan are likely to be disappointed. They base this on three factors: 1) their assumption of a 20% direct tax on gaming revenue, which is not counting corporate tax and additional taxes and fees at the local level that might also apply; 2) the lofty price of entry—operators are talking about investments of $5 billion-$10 billion; and 3) the country’s relatively high construction and labor costs.

“Returns of newer casinos have been falling mainly due to rising capex,” they write. “ROIC (EBITDA/invested capital) in the first year have been falling from as high as >100% (Sands Macao in 2004) to the recent 10-15% for Sands Cotai Central in Macau and Solaire in the Philippines (15%). With lower expected unit productivity in Japan, limited VIP/Chinese penetration and high capex, the casinos could generate lower returns.”